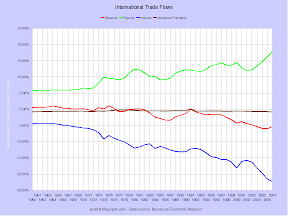

There seems to have been a bit of blogburst over the past few weeks on the implications of collapsing consumer demand and potential inflation in America on the international trade system as it currently operates. There is always some background chatter on the trade deficit, but it seems to have become louder, perhaps prompted by China's apparent desire to depress the renminbi against the dollar in order to keep it's faltering export-led economy as juiced as possible.

The trade deficit is an old hobby-horse of mine, one that I don't ride much because with the dot.com boom and the real estate bubble keeping money (or debt) flowing freely, most people didn't give a damn. Cheap crap for everybody - hurray! But the imbalance has been steadily growing for years, blowing past big, leaving huge in the dust, and reaching colossal proportions without undue effort. And with the rest of the economy in the crapper, a lot more of people are finally realizing that we have a problem.

The trade deficit is an old hobby-horse of mine, one that I don't ride much because with the dot.com boom and the real estate bubble keeping money (or debt) flowing freely, most people didn't give a damn. Cheap crap for everybody - hurray! But the imbalance has been steadily growing for years, blowing past big, leaving huge in the dust, and reaching colossal proportions without undue effort. And with the rest of the economy in the crapper, a lot more of people are finally realizing that we have a problem.

Concerns about outsourcing and imports are nothing new. For instance, in the 1980s there was a lot of hand-wringing about Japan overtaking America. The concern was overblown, but became a entrenched media narrative because the Japanese were growing market share for a product of particular sensitivity for Americans - the automobile. The shift in purchasing was mostly a home-made problem, but the 1979 oil embargo and a ridiculously strong dollar pushed sales of imports to an even higher rate of increase than they had been in the 1970s. But by late in the decade, with a more reasonably valued dollar, somewhat better leadership in Detroit, and the virtual withdrawal of several European makers, concern faded. The 1990-1991 recession brought overall trade almost back into balance, but then something important happened: China took off.

Concerns about outsourcing and imports are nothing new. For instance, in the 1980s there was a lot of hand-wringing about Japan overtaking America. The concern was overblown, but became a entrenched media narrative because the Japanese were growing market share for a product of particular sensitivity for Americans - the automobile. The shift in purchasing was mostly a home-made problem, but the 1979 oil embargo and a ridiculously strong dollar pushed sales of imports to an even higher rate of increase than they had been in the 1970s. But by late in the decade, with a more reasonably valued dollar, somewhat better leadership in Detroit, and the virtual withdrawal of several European makers, concern faded. The 1990-1991 recession brought overall trade almost back into balance, but then something important happened: China took off.

The phenomenal growth of trade with China was something of a surprise, since much had been made of NAFTA and that "giant sucking sound" from the south early in the decade. True, a lot of manufacturing did end up moving to places like Juarez or Tijuana, where the maquiladores set up shop. European and Japanese companies also set up final assembly plants so as to be inside the NAFTA tariff zone. But unlike East Asian countries, Mexico showed little ability to move up the food chain. It merely provided labor, and as a result it's economy grew much more slowly than places like Korea or Taiwan.

The phenomenal growth of trade with China was something of a surprise, since much had been made of NAFTA and that "giant sucking sound" from the south early in the decade. True, a lot of manufacturing did end up moving to places like Juarez or Tijuana, where the maquiladores set up shop. European and Japanese companies also set up final assembly plants so as to be inside the NAFTA tariff zone. But unlike East Asian countries, Mexico showed little ability to move up the food chain. It merely provided labor, and as a result it's economy grew much more slowly than places like Korea or Taiwan.

Like Dean Baker, I have long though the Clinton-era strong dollar policy was moronic. The dollar should have been left to find it's own level, or at least not further strengthened with the implicit threat to intervene in currency markets behind pronouncements by government officials on the topic. However, at first glance this somewhat confusing chart (basically, the higher the line the strong the dollar is against that currency, meaning the same dollar can buy more widgets or wine in the foreign currency) doesn't show a radical strengthening. The dollar actually weakened from 1993 to 1995 before returning to the previous level in 1997. But that is unexpected because the US trade deficit was increasing rapidly at the time. Significant trade deficits should have driven the dollar down because the foreign exchange market works like any other commodity market. People with more dollars than they need (exporting countries) are willing to sell them at every lower prices for what they do need, which is local currency. That's the theory, at least.

Like Dean Baker, I have long though the Clinton-era strong dollar policy was moronic. The dollar should have been left to find it's own level, or at least not further strengthened with the implicit threat to intervene in currency markets behind pronouncements by government officials on the topic. However, at first glance this somewhat confusing chart (basically, the higher the line the strong the dollar is against that currency, meaning the same dollar can buy more widgets or wine in the foreign currency) doesn't show a radical strengthening. The dollar actually weakened from 1993 to 1995 before returning to the previous level in 1997. But that is unexpected because the US trade deficit was increasing rapidly at the time. Significant trade deficits should have driven the dollar down because the foreign exchange market works like any other commodity market. People with more dollars than they need (exporting countries) are willing to sell them at every lower prices for what they do need, which is local currency. That's the theory, at least.

But a closer look at the exchange rate graph shows something odd: a perfectly flat exchange rate with China from 1994 until 2004. Unlike other currencies, the renminbi was fixed against the dollar and in 1994 the Chinese significantly devalued it. And on the previous graph the results can be seen: a rapidly increasing trade deficit with China. Trade with other countries stayed roughly flat, at least until 1998. The Asian financial crisis of 1997 made investors flee many emerging market countries to the safe haven of the dollar, thus pushing its value way up. Then trade took off with everyone. So, in the end, I think the strong dollar policy made only a small difference. It was allowing China to fix the renminbi at such a low level that did the most harm.

Whatever the reason, an overvalued currency was good for lots of constituencies in the short term. It became even easier for American businesses to outsource because their investment dollars went farther. It was easier for developing countries to attract capital to expand their economies - and export sectors were the focus of many governments' policies. It allowed advanced exporting countries to continue ignoring their own structural problems. It made consumer goods cheaper for Americans, along with petroleum products, keeping inflation down. It feed the dot.com boom because the deployment of technology became cheaper as overseas manufacturing learned to make ever more sophisticated products. And it put American investment bankers in charge of a huge portion of the world's capital flows. In other words, globalization happened.

Whatever the reason, an overvalued currency was good for lots of constituencies in the short term. It became even easier for American businesses to outsource because their investment dollars went farther. It was easier for developing countries to attract capital to expand their economies - and export sectors were the focus of many governments' policies. It allowed advanced exporting countries to continue ignoring their own structural problems. It made consumer goods cheaper for Americans, along with petroleum products, keeping inflation down. It feed the dot.com boom because the deployment of technology became cheaper as overseas manufacturing learned to make ever more sophisticated products. And it put American investment bankers in charge of a huge portion of the world's capital flows. In other words, globalization happened.

Sounds great, eh?

And it was - for everyone not employed in the American manufacturing sector. As the decade wore on, a whole narrative developed that said the decline of domestic manufacturing was okay, even good. Americans, instead of making stuff, would become "knowledge workers", sending ideas and services around the globe. But that didn't work out as well as planned. The balance on services expanded slowly and the balance on income remained low relative to GDP, but imports of goods exploded.

And it was - for everyone not employed in the American manufacturing sector. As the decade wore on, a whole narrative developed that said the decline of domestic manufacturing was okay, even good. Americans, instead of making stuff, would become "knowledge workers", sending ideas and services around the globe. But that didn't work out as well as planned. The balance on services expanded slowly and the balance on income remained low relative to GDP, but imports of goods exploded.

Front-line production workers got hit the hardest, of course. Even after factoring lower productivity, longer delivery times, and the friction resulting from communication over distance, time and cultural misunderstandings, outsourcing low-skilled jobs to East Asia was cost effective. A wage differential of 20 times or more is hard to overcome, no matter how well American workers are trained and equipped. And once it got rolling, nothing seemed to stop it. That's because the world, and especially China, extend to the US the "mother of all vendor financing deals" for most of the next decade.

The loss of low-value-added jobs making textiles, footwear, and the like shouldn't be mourned all that much. America has been bleeding those jobs for decades anyway. But the total unwillingness to manage the decline of older industries has made the process far more painful than needed. In the past, various tariffs or other barriers were sometimes implemented to protect domestic jobs. The efforts never worked all that well, and by the 1990s that approach had fallen out of favor - except during the 2-3 months before each election. Instead, the government should have weighed in with policies designed to consolidate the industry at hand in an orderly fashion, remove "legacy" costs as much as possible from the survivors, and help regions that were overly-dependent on one industry to attract new jobs before the older industry collapsed. In other words, America should have had some kind of industrial policy - at least for declining industries. Unfortunately, the dominant free-market ideology prevented the development of high-level policy

The loss of low-value-added jobs making textiles, footwear, and the like shouldn't be mourned all that much. America has been bleeding those jobs for decades anyway. But the total unwillingness to manage the decline of older industries has made the process far more painful than needed. In the past, various tariffs or other barriers were sometimes implemented to protect domestic jobs. The efforts never worked all that well, and by the 1990s that approach had fallen out of favor - except during the 2-3 months before each election. Instead, the government should have weighed in with policies designed to consolidate the industry at hand in an orderly fashion, remove "legacy" costs as much as possible from the survivors, and help regions that were overly-dependent on one industry to attract new jobs before the older industry collapsed. In other words, America should have had some kind of industrial policy - at least for declining industries. Unfortunately, the dominant free-market ideology prevented the development of high-level policy

![]() The lack of a national healthcare system made the decline of older industries more likely, as recent news in the auto industry demonstrates. Not only are costs for existing workers higher than in other countries, past promises to provide healthcare for retirees became a significant overhead cost. The steel industry also suffered tremendously due to legacy costs, though in that case pensions were the main burden.

The lack of a national healthcare system made the decline of older industries more likely, as recent news in the auto industry demonstrates. Not only are costs for existing workers higher than in other countries, past promises to provide healthcare for retirees became a significant overhead cost. The steel industry also suffered tremendously due to legacy costs, though in that case pensions were the main burden.

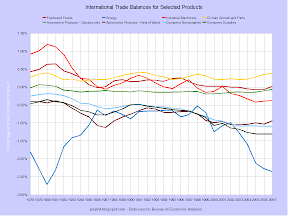

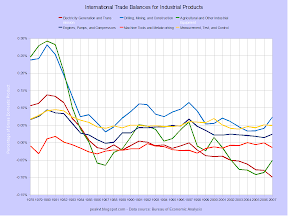

Trends in international trade have not been entirely negative. America continues to be a net exporter of aircraft, locomotives, and parts for each. Balances of trade for industrial products have remained about the same after declining from an artificial high in the late 1970s. The net effect on the economy from the sector is small despite the volumes of trade being quite high.

Trends in international trade have not been entirely negative. America continues to be a net exporter of aircraft, locomotives, and parts for each. Balances of trade for industrial products have remained about the same after declining from an artificial high in the late 1970s. The net effect on the economy from the sector is small despite the volumes of trade being quite high.

No comments:

Post a Comment